For the first time in generations, many people may now need to think about the impact that inflation could have on their retirement income, and to consider whether they can afford to retire yet.

Inflation has climbed to levels not seen for decades and looks set to remain there for the foreseeable future. Various factors will influence how long inflation is with us, but a long-drawn-out Russia/Ukraine conflict would be unlikely to help.

How can we invest to get maximum returns in retirement despite persistent inflation? Here we consider five questions you may need to answer if you’re approaching retirement and want to ensure your portfolios are positioned as well as possible.

What impact could inflation have on your retirement plans?

Firstly, it is important to understand just how much of an impact inflation could have on your income in retirement.

On average, a 65-year-old man retiring today is expected to live for 19 years, while a 65-year-old woman retiring today would be expected to live for 22 years. For those on a fixed retirement income, high inflation can be very damaging.

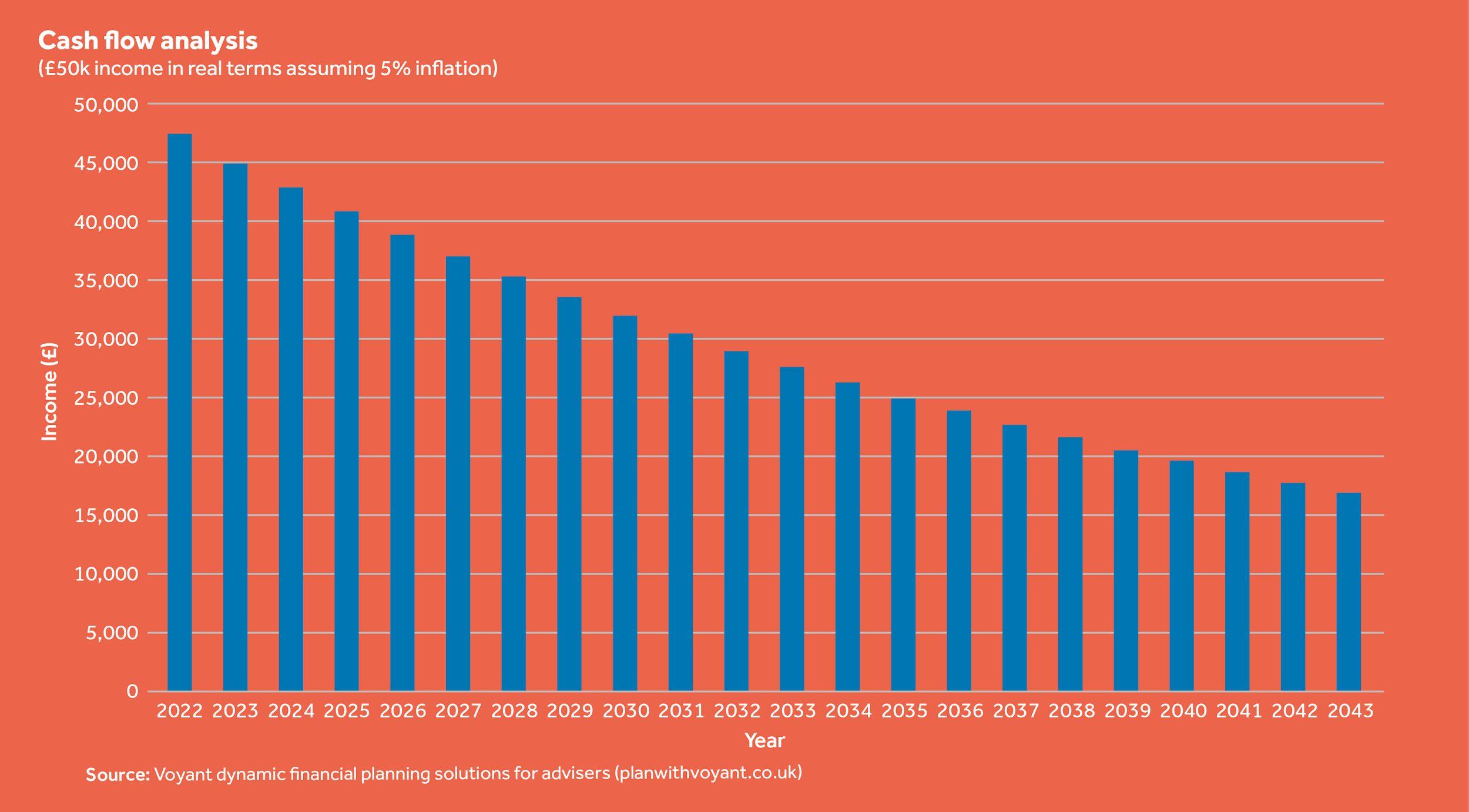

The following graph helps illustrate why: assuming inflation averages 5% pa for 22 years and you have an annual fixed retirement income of £50,000, the effect would be to reduce this figure to marginally over £17,000 per annum by the end of your lifetime.

This means that ensuring retirement income keeps pace with inflation, or preferably grows in ‘real’ terms (i.e., factoring out the effect of inflation), is of utmost importance.

What is your timeline to retirement?

As wealth managers with many years of experience, we know that many people do not start considering whether they have sufficient funds to retire until around 18 months before they plan to stop work. That’s human nature.

However, we believe that ideally, everyone should have a carefully considered investment strategy in place well before their retirement date. As part of this, deciding when you want to retire and having a target date to work towards can be useful.

In the post Covid-19 world, we are finding that many clients have decided to rethink their retirement timelines. Some have decided to retire earlier to spend more time with children or grandchildren, or perhaps to travel abroad again now international borders have reopened. Others have decided to delay their retirement, taking advantage of new ‘hybrid’ working arrangements to continue in their jobs for a little longer.

The good news is that it’s never too late to optimise your investments for retirement, no matter how long you have left until you retire, or if you decide to change your plans.

What is your attitude to risk?

In an investment context, risk is a measure of the extent by which investment returns may deviate from expectations. A key factor in investment decisions is establishing the level of risk that is acceptable to each individual client, as this differs widely from one person to another. Your Canaccord wealth manager will spend time understanding your unique situation and help you to assess the most appropriate risk level for you.

We will then manage your portfolio to match your risk appetite. This will generally mean a different asset allocation between equities, bonds, property and other alternatives, with a view to ensuring that the income derived from that portfolio can at least keep pace with inflation.

Are you sitting on too much cash?

One of the best ways to protect against inflation in retirement is by investing in ‘real assets’ – i.e., any investment other than cash. This is because whenever inflation rates are higher than interest rates (as they are at the moment by quite some margin), the value of cash is guaranteed to fall in real terms.

Exactly which real assets would be appropriate for you will need careful consideration. Clients looking for more income-generating investments would potentially look at a different blend of asset classes to someone looking for more capital growth, for example. When deciding how best to invest your excess cash for your unique circumstances, it is always a good idea to seek professional guidance.

Could your home be a retirement asset?

Property values in general have risen above inflation over the last 30 years. However, many clients heading towards retirement realise that while their main residence may be one of their most valuable assets, it provides them with no income. Some may look to downsize in order to free up additional funds to assist them in retirement, or consult a specialist on whether other options could be appropriate for them.

In summary

With inflation raising its head for the first time in many years, clients approaching retirement are having to grapple with some new challenges. There is no ‘one solution’ to solve these problems, but forward planning is imperative for a comfortable retirement in an inflationary world.

Written by Chris Colclough, Head of Wealth Management, Guernsey, at Canaccord Genuity Wealth Management.

The information contained on this website and any resources available are not intended as, and shall not be understood or construed as, legal advice. The publisher is not an attorney, accountant or financial advisor, nor are they holding themselves out to be, and the information contained on this website is not a substitute for advice from a professional who is aware of the facts and circumstances of your individual situation.

{kind=link}