Mark Clubb, Executive Chairman of TEAM plc, discusses the ‘red flags’ flying in these challenging times. There is fear out there.

Investors are concerned if not frightened about rising inflation, interest rates, war in Europe, and the possibility of the global economy entering a recession. The sharp fall in stock markets have compounded that. I don’t see this volatility going away any time soon. But there is always opportunity.

However, first we need to identify the red flags. Then we can examine what impact these have on markets to then position our investment portfolios appropriately.

However, first we need to identify the red flags. Then we can examine what impact these have on markets to then position our investment portfolios appropriately.

This year is turning out to be crazy crazy. It seems to be an endless cycle of bad news. Even before the horrors of Russia’s actions, the surge in inflation had resulted in fears of rising interest rates sending all major stock markets into correction territory.

But despite all of this … Do… Not… Panic.

The most important thing we must do is continue to educate ourselves despite how bad things appear.

Let’s start with a list of ‘impacts’:

- Energy prices (oil and gas) likely to remain high, prolonging inflation

- Food prices likely to remain higher given that Russia and Ukraine are circa 25% of global wheat production or exports.

- Global supply chain blockages and shortages worsen, particularly for those products reliant on Russia/Ukraine. Further supply shock induced inflation.

- Continued labour market disruptions and shortages in Europe and UK particularly. Increased wage inflation pressures.

- Heightened cyber risks.

- Growth in activist sponsored demands leading to divestments of inappropriate assets such as Russian together with financial help or assistance for Ukrainian refugees.

Now a list of implications:

- Increased spending on defence.

- Increased controls on trade such as exports and imports together with heightened incidence of sanctions. Move towards a protectionist world and further deglobalisation. Added risk to global growth and bad news for emerging economies.

- Increased U.S. repatriation of manufacture/assembly. ‘Made in America’.

- The above slows China economy and further contains China/U.S. tensions. Negative for China and emerging economies.

- Increased cyber security legislation and business demands.

- Cryptocurrency regulation and much more aggressive oversight.

- Increase in gas and oil investment approvals.

- Likely increase in global investment flows into the U.S. Dollar (safer haven). Strong dollar not positive for emerging economies.

- More aggressive oversight and possible legislation for social media.

- China will rein back global territorial ambitions. The ‘Free World’ reaction to the invasion of Ukraine despite downside risks to the economies could imply the same for an invasion of Taiwan or such like China initiative.

The sanctions against Russian Central Bank have been unexpected and massively powerful. China will work towards reducing the risk of a similar fate.

Some negatives:

- Slowdown in decarbonization initiatives and spending.

- However, broader spending such as defence and social worsens inflation picture.

- Potential for corporate tax increases.

- But the biggest is: The much-increased likelihood of a global recession.

Recession causes pain. But for those that are prepared, times like these are potentially wealth-generators when looked at in the rear view mirror of time.

Yes, it’s scary but if we act wisely in the midst of today’s heightened volatility, portfolios will be in vastly better shape when all of this is eventually behind us. At TEAM we always look to be tactical in our approach.

Some things to do

First be exposed to oil, gas and broader commodities. We expect continued volatility in food and energy prices. At some point that will seep into the price of other goods and services.

Here are just a few products that are made with petroleum:

Solvents, ink, upholstery, bike tires, deodorant, elastic, shoe polish, soap, football boot studs, motorcycle helmets, cortisone, life jackets, paint, skis, storage racks, hand lotion, luggage, antifreeze, shower curtains… and there’s loads more.

So red flags for companies in fuel or oil intensive sectors (e.g., airlines, construction, plastics manufacturers). Caution for other commodity intensive input costs.

These red flags keep waving until something happens that ends this current supply/demand imbalance. To forecast this is speculation.

Where’s the silver lining?

The common preconception is that recessions and bear markets go hand-in-hand. But they don’t always. By the way, oil or energy price spikes have preceded almost every recession of the last 80 years. In fact, ‘normal’ recessions don’t necessarily lead to bear markets. In the early 1980s, a U.S. economic recession led to just a 15% fall in the S&P. The early 1990s recession similarly led to just an 18% fall.

Against the above, early 2000s recessions resulted in a 40% stock market collapse, while the 2008 financial crisis induced recession torpedoed stocks by 50%.

However, if we do head into a recession in 2022/23, and it is a more ‘normal’ recession, like the early 1980s and early 1990s, in which stocks dropped less than 20% then there is light. The S&P 500 is already more than 10% off recent highs. Therefore, history says that even if we enter a recession, shares maybe only fall another 5% to 10% from current levels.

That’s not much further downside, and it means that now may be the time to start buying into equities and that’s what many ‘insiders’ are suddenly doing.

This is a dramatic change to when the market and share prices were falling in December, January, and most of February.

Since the last week of February, insiders at many of the U.S. growth companies have been on an enormous buying spree. With insiders buying into this fallen market maybe we should be too. In total more than 30 corporate insiders have bought over $290 million worth of stock across 27 different growth companies I looked at in past two weeks alone.

Companies have been buying too

We are also witnessing huge share buyback programs being approved, increased and part executed.

Last week Amazon announced a $10 billion share buyback program. Applied Materials announced a $6 billion buyback plan.

Two weeks ago, Advanced Micro Devices launched its $8 billion buyback program. Cisco meanwhile, has expanded its buyback by $15 billion, and Meta bought back around $6 billion of its stock in January alone.

Buybacks are expected to continue at a higher level for Q1 2022, even as prices have declined, as reduced prices will increase the number of shares purchased and lift earnings-per-share due to share reduction. Companies tend to approve new buyback programs or significantly expand current ones when the directors think the share price is undervalued. Maybe we should too?

Just a reminder. After the Covid-19 stock market collapse of March 2020, there was a huge acceleration of insider buying in late March and early April which coincided with the bottom of that crash.

I would start with solid growth companies that will continue to grow their revenues and earnings at a very healthy rate over the next several years.

Focus on cyber security

Maybe focus on such growth companies exposed to the above impacts and implications such as cyber security.

According to Gartner, worldwide spending on cyber security has grown by circa 9% per year since 2014. Further:

- Cybersecurity spending was just 3.5% of IT budgets in 2021.

- Cyber spending growth has consistently accelerated over the past few years, as the need for security solutions has become increasingly required. In 2021, it grew by more than 12%. It is expected to grow another 12% in 2022 and this was before the Russian invasion.

Cyber security could easily be 6% of IT budgets by 2030 and 8% of IT budgets by 2040. This could mean 11% annualized growth in spending throughout the 2020s and 8% annualized growth through the 2030s.

In other words, this industry is just getting started and shares like industry leader an TEAM International Equity Fund holding, Crowdstrike have been down as much as 21% since the beginning of the year. Maybe also some of the other leading technology companies like Alphabet and Microsoft or leading healthcare companies.

Yes, things could grow worse for the global economy and the stock market. However, these leaders are still going to be innovating, changing our world, and generating long-term wealth for their shareholders and investors.

Look at the dividends

The last area I would recommend looking to invest in for these times, whether we have a recession and/or bear market or not is dividends and income. No one should underestimate the hidden power of companies that grow their dividends.

Dividends provide a ‘guaranteed’ return that can supplement your income, act as a buffer against market volatility, and provide protection against inflation. It can also be cashflow to be invested at lower prices. The power of compounding or dividend reinvestment practice.

However, it’s easy to lose sight of their importance during roaring bull markets like we’ve experienced in recent years. Now more than ever, it’s important to own shares in high-quality companies that pay consistent dividends. Yes, the above share buybacks help too. But dividends give you the flexibility to either reinvest or generate income for other purposes.

Research shows dividends have accounted for roughly 40% of the broad U.S. stock market returns over the long run. This jumps to as high as 70% or more for entire decades during the prolonged bear markets.

Dividends can provide a great boost to your returns when things are going well but they become absolutely critical for making money in shares when trouble sets in. And that’s especially true during times of high inflation, like we’re experiencing now.

There’s further good news on this front. S&P 500 Q3 2021 dividends increased 3.0% to a record $133.9 billion from Q3 2021’s $130.0 billion and were 10.1% greater than the $121.6 billion in Q4 2020. For 2021, dividends were a record $511.2 billion, up 5.8% on an aggregate basis from 2020’s $483.2 billion. (http://www.spdji.com/indice)

This hidden power of dividends is well demonstrated by our TEAM Diversified Income Model portfolio. Year to date the overall portfolio is down 1.99% and will produce over 4% gross income yield.

Just don’t make the mistake of ‘chasing yield’. Many investors are tempted to buy stocks with the highest dividend yields. In fact, often those ultra-high dividend payers or yielding shares indicate another big red flag. They can indicate that the dividend isn’t sustainable and is at risk of being reduced or eliminated completely.

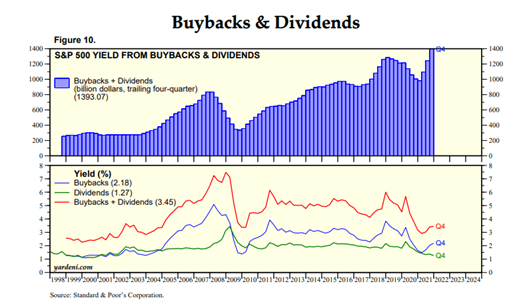

The key is to choose companies that pay sustainable growing dividends. When you add dividends to share buybacks in the S&P500 you get the following: S&P 500 Yield From Buybacks and Dividends = 3.45%

This is looking more and more like an opportunity for investors with more than a 2-year time horizon. You are being paid on average 3.45% for taking the risk in buying equities.

The information contained on this website and any resources available are not intended as, and shall not be understood or construed as, financial advice. The publisher is not an attorney, accountant or financial advisor, nor are they holding themselves out to be, and the information contained on this website is not a substitute for financial advice from a professional who is aware of the facts and circumstances of your individual situation.

{kind=link}